Many factors impact executive compensation programs today. As a compensation manager, your executive compensation plan should be focused on the alignment of pay and performance metrics with pay programs influenced by multiple factors.

Key Takeaways for Designing Executive Compensation Plans:

- Communication internally and externally is key

- Always set appropriate goals and expectations

- Look backward towards historical levels of performance

- Look forward to future projections of performance

- Examine industry averages

- Examine competitor plans where data is available

- Revisit the plan as the organization evolves

- Build in governance from the start

What is Executive Compensation?

Executive compensation differs significantly from traditional pay structures for hourly or salaried employees. Unlike standard compensation, executives and other senior leaders receive pay that is heavily weighted toward incentives tied to real performance and measurable results.

When an organization underperforms, executives typically see their total compensation fall well below target levels, often reduced to a fraction of their potential earnings. Conversely, when an organization meets or exceeds its annual goals, and long-term value grows, executives are rewarded substantially above their base targets.

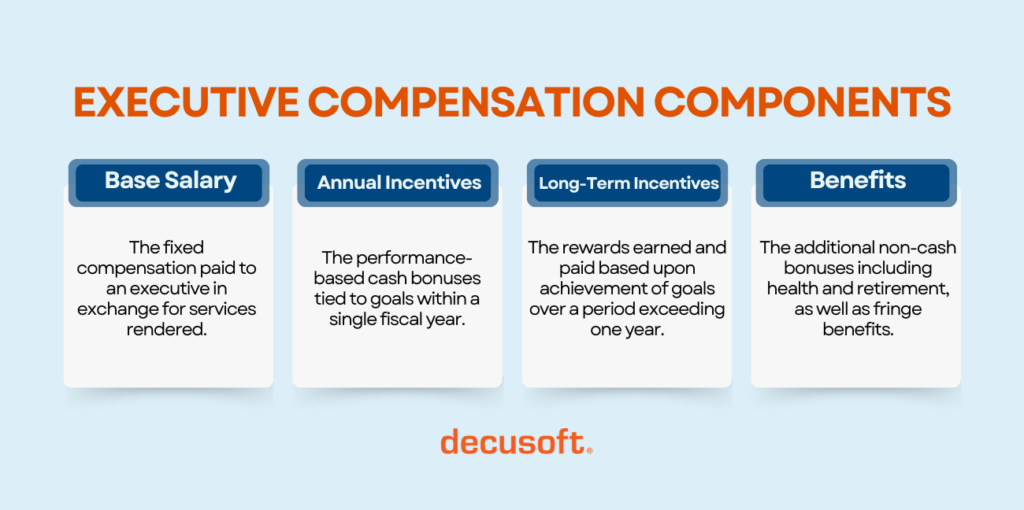

Compensation packages for senior executives consist of a few basic components:

- Base salary

- Annual incentives / annual bonuses

- Long-term incentives

- Benefits and perquisites

Components of Executive Compensation

Base Salary

Base salary is fixed compensation paid to an executive in exchange for services rendered. It provides a stable source of income regardless of the remaining compensation package, and is typically established at the start of an employment relationship or reviewed annually.

While the base salary generally represents a small percentage of total compensation for executives, annual and long-term incentive targets are frequently expressed as a percentage of base salary, so even modest salary adjustments ripple across the entire pay program.

How to Determine Base Salary for Executives

Setting base salary starts with market data. Organizations should benchmark the role against relevant industry surveys, peer company proxy disclosures where available, and third-party compensation databases to understand what the market is paying for comparable positions. From there, internal factors come into play: the executive’s experience, tenure, scope of responsibility, and performance history all influence where within a salary range the individual should be positioned. Most companies target the median of their relevant market as a starting point, with flexibility to go above or below based on the factors above.

Decusoft’s Predictive Compensation pulls from real-time, publicly available data sources including CPI-U for cost-of-living, online industry salary reports, and government databases like the U.S. Bureau of Labor Statistics, giving compensation teams current market context without additional research. Every recommendation comes with low, medium, and high options, giving managers a structured range to work within rather than a single figure to accept or reject.

Annual Incentives / Short-Term Bonuses

Annual incentives, also called short-term incentives (STI), are performance-based bonuses tied to goals within a single fiscal year. These cash bonuses are structured around predetermined metrics, which may include financial targets like revenue growth, EBITDA, or earnings per share, as well as operational or strategic objectives.

Targets are defined as a percentage of base salary and should reflect market opportunity for the position and internal pay equity. In a well-designed program, they also support the company’s long-term business strategy. Payouts vary based on actual performance relative to target, with above-target bonuses when goals are exceeded and reduced or no payout when they are not.

How to Set Annual Incentives for Executives

Goal setting is the most complex aspect of incentive program design. Goals should be realistic, motivational, and tied to the board-approved business plan and budget.

Most annual incentive plans are structured around three payout levels:

- Minimum: The lowest performance level at which a bonus is earned, typically paying out at 25-50% of target.

- Target: The expected or budgeted level of achievement, paying out at 100% of target.

- Maximum: Exceptional performance, typically capped at 150-200% of base salary to discourage overly aggressive behavior

As a general rule of thumb, executives should hit the minimum threshold at least 90% of the time and meet the maximum targets roughly 10% of the time. This means that 9 of 10 years, the executive is hitting the minimum threshold, and 1 of 10 years, the executive is hitting the maximum. The other 8 years are somewhere in the target range. If executives consistently hit maximum, goals may not be rigorous enough. If they consistently fall below minimum, goals may be unrealistic or incentives may not be motivating enough.

It is worth monitoring what competitors and peers are offering. Industry standards should not dictate your plan, but ignoring them entirely can lead to surprises in recruiting and retention.

Long-Term Incentives for Executives

Long-term incentives (LTI) are rewards earned and paid based upon achievement of goals over a period exceeding one year. This is one of the most important aspects of executive compensation programs. For most top executives, LTI represents the largest component of total compensation. Usually, 50-60% of an executive’s pay is based on long-term performance.

The purpose of long-term incentives is to:

- Align executive and shareholder interests

- Attract, retain, and motivate top talent

- Focus participants on critical performance criteria

- Provide competitive pay opportunities based on performance

- Create wealth for executives tied to company success

Types of Long-Term Incentives for Executives

There are three main forms of long-term incentives used in executive compensation: appreciation vehicles, time-vested full value vehicles, and performance-vested vehicles.

Appreciation Vehicles: Stock Options and SARs

Stock options give executives the right to purchase company shares at a set price (the exercise price) during a specified period.

For example, an executive might receive options to purchase 1,000 shares at $50 per share. If the stock rises to $60, the executive can buy at $50 and capture the $10 gain per share.

Stock-settled appreciation rights (SARs) work similarly, but instead of purchasing shares, the executive receives only the profit in shares when the award is exercised.

Time-Vested Full Value Vehicles: Restricted Stock and RSUs

Restricted stock units (RSUs) represent a promise to deliver shares contingent on meeting a required service period, typically three to four years.

For example, an executive granted 1,000 RSUs on a four-year vesting schedule would receive 250 shares at the end of each year, regardless of company performance.

Performance-Vested Vehicles: Performance Shares and PSUs

Performance shares and PSUs function similarly to RSUs but require the executive to meet defined performance goals in addition to a service period. They are viewed favorably by shareholders and advisory firms because of their direct focus on results.

For example, an executive might receive 1,000 PSUs that vest only if the company achieves a 10% revenue growth target over three years.

Other Key Considerations

- IRC Section 162(m): Stock options and performance-vested shares may qualify as performance-based compensation. Restricted stock generally does not.

- Change in Control: Standard practice has shifted from automatic accelerated vesting (single-trigger) to requiring job loss as a condition (double-trigger).

- Share Ownership Guidelines: Most firms require executives to hold stock valued at a multiple of base salary, typically 6x for CEOs and 1-3x for direct reports. Options and performance-vested shares are generally not counted toward these guidelines.

- Clawbacks: Most governance frameworks require companies to recoup incentive compensation if the performance it was based on is later found to be inaccurate. Policies will need updating once Dodd-Frank regulations are finalized.

How to Determine Incentive Programs For Executives

Choosing the right LTI vehicles starts with understanding what the organization is trying to accomplish. Companies focused on retention may lean toward RSUs with time-based vesting, while companies focused on performance alignment may favor PSUs tied to financial or operational metrics. The mix of vehicles, vesting schedules, and award sizes should also be benchmarked against peer companies and industry norms to stay competitive. For public companies, proxy disclosures from direct competitors are a useful reference point. Award sizes should also account for current market conditions, including equity valuations and the competitive landscape for executive talent.

Use compensation management tools to assist in the planning and management of long-term incentives.

Benefits and Perquisites

Benefits for executives often mirror the non-financial benefits offered to the broader employee population, including health insurance, retirement benefits, and paid time off, though these are frequently enhanced in scope or value. Perquisites, sometimes called fringe benefits, are additional privileges granted specifically to senior executives and may include company vehicles, club memberships, financial planning services, executive life insurance, or a Supplemental Executive Retirement Plan (SERP). While perks represent a small portion of total compensation, they play a real role in attracting and retaining executive talent.

How to Determine Benefits and Perquisites for Executives

Beyond the base benefits, perquisites should be tied to two things: market practice and business rationale. Review what peer companies and direct competitors are offering at the executive level. If a perquisite is common in your industry, excluding it can put you at a disadvantage when recruiting. If it is uncommon, offering it may not move the needle on attraction or retention.

Business rationale matters as well. Perquisites that support executive productivity and health, such as financial planning services, executive physicals, or travel-related benefits, are generally viewed more favorably by shareholders than purely personal perks. Shareholders and proxy advisory firms scrutinize perquisites closely, and those that appear excessive or disconnected from business purpose tend to draw criticism.

A few practical guidelines:

- Benchmark perquisites against peer companies and industry norms

- Prioritize perquisites with a clear link to executive productivity or retention

- Avoid perquisites that could attract negative attention from shareholders or advisory firms

- Review the full perquisites package any time executive contracts are renegotiated or market data is updated

Objectives of Compensation Management

The core objectives of any executive compensation program come down to four things: attracting, motivating, retaining, and aligning. Organizations need to bring in the right leadership talent, keep them engaged, hold onto them over time, and make sure their financial interests are tied to the performance of the business.

Pay Mix

Executive compensation is not a single number. It is a mix of fixed and variable pay, short and long-term incentives, and cash versus equity. The right mix depends on the organization, the role, and the stage of the business. A company prioritizing retention may weight long-term equity more heavily. A company in a high-growth phase may lean into performance-based short-term incentives. Pay mix should be revisited as the organization evolves.

Market Competitiveness

Every organization needs to define what being competitive means for them. Competitive compensation packages are most often benchmarked to the median of the relevant market, but that is a starting point, not a rule. High-demand roles, specialized business units, or departments driving new growth may warrant compensation structures that sit above market median to attract the right talent. The key is flexibility. A compensation program that works well for a traditional corporate function may not be the right fit for a new product development team or an emerging business unit. Build in the ability to adjust, and benchmark regularly against peers and competitors to stay informed.

Internal Pay Equity

Market competitiveness matters, but so does how executive pay relates to the rest of the organization. Internal pay equity looks at whether compensation is fair and consistent relative to role, responsibility, and performance across the company. Organizations that ignore internal equity risk damaging morale and trust, particularly as pay transparency becomes more common. A well-structured executive compensation program should be defensible not just to shareholders, but to the broader employee population.

Talent Retention

Attracting executives is only half the challenge. Keeping them is the other. Long-term incentives with multi-year vesting schedules, competitive benefits, and clearly defined paths to wealth creation all play a role in retaining top leadership talent. When executives leave, the cost extends well beyond recruiting. Organizational knowledge, relationships, and strategic continuity all walk out the door with them.

Public Reporting and Regulations (Public Companies)

For publicly traded companies, executive compensation is subject to significant regulatory oversight and disclosure requirements. The SEC requires companies to disclose executive pay in proxy statements, including detailed breakdowns of salary, bonuses, equity awards, and perquisites. Say-on-pay votes give shareholders a direct voice in compensation decisions, and proxy advisory firms like ISS and Glass Lewis publish recommendations that carry real influence. Public companies must design compensation programs with these audiences in mind, not just their internal stakeholders.

Final Thoughts on Executive Compensation

Executive compensation is a difficult topic to get right. There are dozens of variables to consider and numerous performance indicators to weigh when developing an executive compensation package. With a well-designed plan, your organization can attract top talent and properly incentivize your management team, and position the company for long-term success.

Decusoft’s Compose platform is built to manage any type of compensation plan, including executive and deferred compensation, STI and LTI, equity, stock, and more, all within a single system. From real-time reporting and scenario modeling to automated workflows and built-in validations, Compose gives HR and finance leaders the tools to run a faster, more transparent compensation process from start to finish.

See how Decusoft supports executive compensation programs.