Long-term incentives are earned based on the achievement of goals over an extended period, typically tied to stock price performance or business results. LTIPs function as a long-term investment for both the company and the employee, with returns linked to hitting performance targets and driving company growth.

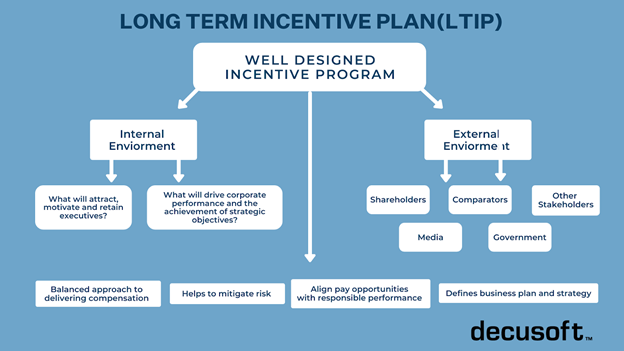

When designing or evaluating an LTIP, it helps to take a holistic view of compensation. Consider the balance between short-term and long-term rewards, cash versus equity, and the types of vehicles you’re using. The goal is to determine what will attract, motivate, and retain executives while driving organizational success and supporting the company’s strategic objectives.

There are a few design factors to keep in mind, whether you’re building a new incentive plan or modifying an existing one. LTIPs typically involve an earning process that is deferred over time, with a vesting schedule and delayed payouts that encourage retention. Knowing which success metrics drive the right expectations and behaviors is critical, and compensation options should be balanced with responsible outcomes that reduce organizational risk.

Two major types of LTIP vehicles include appreciation-based awards and time-based awards, which are detailed later in this article.

While LTIPs have traditionally been reserved for executive-level employees, there is a growing trend to extend these plans to other key contributors. They help attract skilled recruits, retain top talent in competitive markets, and reduce turnover by incentivizing long-term commitment.

Glossary of Long-Term Incentive Plan Terms

Vesting Period/Schedule: The timeframe a corporation sets that determines when an individual can assume full ownership of an asset, usually equity options or retirement funds.

Cliff Vesting: A vesting schedule where the individual receives the full reward at once rather than incrementally over time.

Gradual Vesting: Vesting that occurs over time, with a set proportion of the award vesting each year. It’s common for nothing to vest during the first several years, with increasing percentages vesting in subsequent years until the award is fully vested.

RSUs (Restricted Stock Units): A commitment from an employer to issue a certain number of shares at a future date. Since the recipient doesn’t hold the stock immediately, RSUs carry no voting rights until shares are delivered.

Restricted Equity Awards: Similar to RSUs, except the recipient owns the stock and has voting rights immediately upon grant.

Employee Stock Option (ESO): A grant allowing an individual to purchase a set number of shares at a predetermined price at a future date. If the stock price exceeds the exercise price when the employee is ready to buy, they benefit from the difference. Employees don’t need to wait for all shares to vest before exercising; they can exercise any vested portion at any time. Exercising when the stock price is below the set price would not be advantageous.

Performance-Based LTI (PSUs): The right to receive shares in the future, contingent upon achieving specific performance goals and meeting a requisite service period. Similar to time-vested restricted stock, but with a performance condition tied to company results.

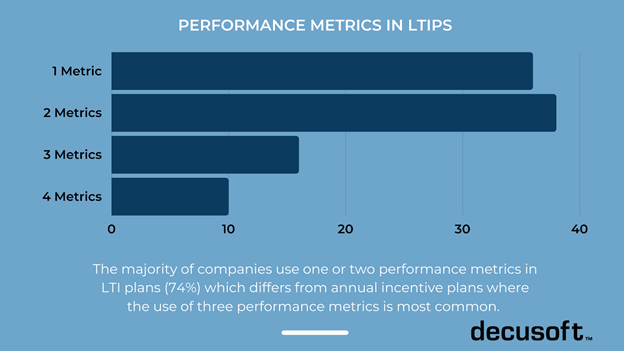

Performance Metrics: Measures that should be aligned with business strategy and reflect the key drivers of corporate and shareholder value. Effective metrics create a clear line of sight for key employees, focusing their efforts and mapping their accountability.

Absolute Metrics: Rely on the ability to forecast future results. These may not always be well-received by investors due to the difficulty of accurate long-term forecasting.

Relative Metrics: Dependent on how performance compares to a peer group. These can serve as useful benchmarks when absolute performance is difficult to predict, but carry the risk of payouts for negative performance that is merely “less poor” than comparators.

The majority of companies (78%) include a relative TSR measure in performance metrics, and most (91%) pair TSR with at least one other performance measure.

Relative TSR: One of the most prevalent metrics in LTI programs. Relative TSR is viewed favorably by shareholders and advisory firms, and is useful when absolute performance is hard to predict. However, it’s not directly within management’s control, the “Phoenix effect” can penalize steady performers, and selecting the right comparator group is critical. Expense is recognized even if the award is not earned.

Long-Term Incentive Types

Appreciation Vehicles

Stock Options: The right to purchase shares of company stock at a specified exercise price during a defined term. Stock options provide strong alignment with shareholders, are easy to communicate, and represent a fixed expense. However, they may not be viewed as performance-based since they aren’t tied explicitly to company financial performance, and they present the possibility for dilution.

Stock Appreciation Rights (SARs): Similar to stock options but less dilutive, SARs are linked to stock value appreciation and offer specific tax benefits along with associated risks.

Time-Vested Full Value Vehicles

Restricted Stock / Restricted Stock Units (RSUs): The grant of shares (or promise to grant shares, in the case of RSUs) contingent on meeting a requisite service period. These have strong retention value, are popular with employees and shareholders, are less dilutive than traditional stock options, and represent a fixed expense. The main criticism is that they’re sometimes viewed as “pay for pulse” since they aren’t tied to company financial performance.

Performance-Vested Vehicles

Performance Shares / Performance Share Units (PSUs): Shares (or the promise to receive shares) contingent upon hitting specific targets and achieving associated performance goals while meeting the requisite service period. PSUs provide a strong focus on performance and shareholder alignment, and they are popular with advisory firms. They are a fixed expense and may be subject to reversal if performance goals aren’t met.

The main challenge with performance-vested awards is setting the right criteria. Poor goal setting may lead to a perception that the awards are less valuable, and expense reversal is not possible for awards earned based on market conditions like share price or TSR.

Cash-Based Awards: A popular long-term incentive for private companies that have limited liquidity and more complicated equity valuations.

Key Takeaway: Types of long-term incentives include appreciation vehicles (stock options and SARs), time-vested full value vehicles (restricted stock/RSUs), and performance-vested vehicles (PSUs). Each type serves a different purpose in aligning employee interests with company outcomes.

When Do Workers Earn Long-Term Incentive Plan Benefits?

Most LTIPs span three to five years before employees receive the full value of the reward. Depending on the award’s vesting schedule, individuals typically cannot earn the entire reward at once. Full-value awards vest based on time, requiring the employee to remain with the company over the specified period.

This article focuses primarily on equity-based awards, which are the most common type of long-term award in public companies, though a small number of firms use cash-based plans as well.

Key Takeaway: Most long-term incentive plans span three to five years before the employee receives the full value of the reward.

What Are the Various Forms of Long-Term Incentive Plans Available?

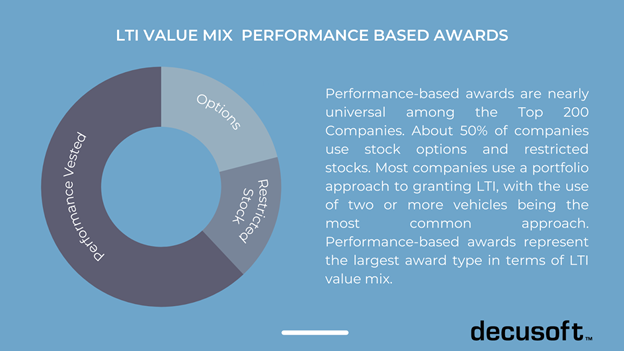

The majority of companies use options and performance-based awards as part of their LTI program. Among the Top 200 Companies, performance-based awards are nearly universal, requiring employees to hit specific targets to receive their payouts. This directly aligns employee goals with shareholder interests. Payouts are often tied to milestones such as Total Shareholder Return (TSR), revenue growth, or earnings per share (EPS).

About 50% of companies use stock options and restricted stocks, and most take a portfolio approach to LTI by granting two or more vehicle types. Performance-based awards represent the largest award type in terms of overall LTI value mix.

Key Takeaway: Most companies use restricted stock options and performance-based awards. Performance-based awards are nearly universal across the top 200 largest publicly traded companies.

Key Considerations in LTIP Design

Align with strategy. Your LTIP should directly support the company’s long-term business objectives and shareholder value creation.

Balance is crucial. Consider the right mix of short-term and long-term vehicles, cash and equity, and retention versus performance orientation.

Reevaluate regularly. Market conditions, company strategy, and regulatory requirements change. Your LTIP should evolve accordingly.

Understand the ramifications of change. Modifying an existing plan can have tax, accounting, and employee relations implications. Assess these before making adjustments.

Assess risk. Consider the potential for unintended consequences, dilution, and the message your plan sends to shareholders and advisory firms.

Communicate clearly and often. Transparent communication about plan structure, vesting, performance criteria, and tax implications builds trust and helps employees understand the full value of their compensation.

Don’t follow the herd. What works for a competitor may not work for your organization. Design your plan around your specific strategy, culture, and workforce needs.

Pitfalls to Avoid in LTIP Design

Before finalizing any LTIP, it’s important to be aware of common design mistakes that can draw scrutiny from shareholders, advisory firms, and regulators.

Pay-for-Performance Misalignment: This occurs when the majority of equity awards aren’t performance-based, when target LTI awards increase in years of poor corporate or stock price performance, when payouts happen in years where TSR has declined, or when dividends on unearned or unvested shares are paid out.

Size and Concentration of Awards: Large sign-on, retention, or other one-off awards outside the annual program can raise flags. Similarly, if the CEO and other proxy officers receive an outsized portion of grants relative to all employee awards, advisory firms will take notice.

Performance Metric Issues: Using the same metric for both short-term and long-term incentives is often viewed as “double-dipping.” Discretion in payouts is generally seen negatively, and relying on a single, non-relative metric is likely to be problematic.

Design Parameters: One-year performance periods in a “long-term” plan undermine the plan’s purpose. Other red flags include large or uncapped upside potential, no ownership guidelines or holding requirements, no clawback policy, and single-trigger vesting of equity awards upon a change in control, which is a significant concern for shareholders and advisory firms.

Key Takeaway: Avoid pay-for-performance misalignment, “double-dipping” on metrics, and missing governance safeguards like clawback policies and ownership guidelines.

The External Environment and LTIPs

External factors play an important role in shaping LTIP design. The media maintains a close focus on executive pay, and perceived disparities in publicly traded firms regularly draw scrutiny. When building an LTIP, it’s worth asking how the plan will be received publicly.

Government regulations also carry significant weight. “Say on Pay” rules and proposed pay-for-performance regulations affect how companies structure executive compensation. Staying current with legal and compliance requirements is essential.

Competitor analysis matters as well. Many companies are refining their equity plans to be more performance-focused, largely because shareholders and investors are paying close attention to these metrics. Understanding what comparable organizations offer helps ensure your plan remains competitive within your industry.

Key Takeaway: External factors including media perception, government regulations, and competitor practices are important considerations when designing a long-term incentive plan.

Tax Implications of Long-Term Incentive Plans

LTIPs are powerful tools for motivating employees and driving company performance, but they come with important tax considerations for both employers and employees.

For employees, the timing and type of award determine when and how much ordinary income tax is owed. Stock options are generally taxed when exercised, with the difference between the exercise price and market value treated as ordinary income.

- Restricted stock is typically taxed upon vesting when employees receive full ownership.

- Cash-based awards are taxed as ordinary income when paid out.

- Vesting schedules and performance targets influence the timing of taxation, which affects the net value employees receive.

Private companies face unique challenges, particularly around ownership dilution when granting equity-based awards. They need to balance rewarding key employees with the impact on company ownership and control. Public companies must navigate additional accounting and disclosure requirements to ensure LTIP compliance while supporting shareholder value.

On the employer side, companies can often deduct the value of awards granted or vested, but deductions may be limited based on performance targets, vesting schedules, and award type. Certain tax rules limit deductions for compensation paid to senior executives, especially in public companies.

Best Practices for Tax-Efficient LTIP Design

Design with tax efficiency in mind. Structure LTIPs to minimize tax liabilities for both the company and employees. This may involve tax-deferred vehicles, carefully selecting award types, or timing grants to take advantage of favorable tax treatment.

Communicate tax implications clearly. Employees should understand when they may owe taxes, how much they might owe, and what choices they have. Transparent communication helps employees appreciate the true value of their incentives.

Monitor changing tax laws. Tax regulations affecting LTIPs can shift, especially for public companies. Review and update your plan regularly, adjusting vesting schedules or award types as needed.

Balance company and employee interests. Consider how tax implications affect retention and satisfaction. Well-designed LTIPs align employee interests with company goals and support growth over multiple years.

Simplify LTIP Management with Decusoft Compose

Managing the complexity of long-term incentive plans across your organization requires more than spreadsheets and manual tracking. From vesting schedules and performance milestones to tax considerations and board reporting, the administrative burden of LTIP management can consume significant time and resources while increasing the risk of costly errors.

Decusoft Compose is a compensation management platform built to handle this complexity. Compose enables HR and finance teams to plan, model, and administer LTIPs alongside every other component of your compensation program in a single, secure system. With no-code configurability, real-time reporting dashboards, and AI-powered insights, Compose gives your team the tools to manage even the most sophisticated incentive structures with accuracy and confidence.

Whether you’re tracking equity grants, modeling payout scenarios, or preparing board-ready reports, Compose streamlines the entire process so you can focus on strategy instead of administration.

Schedule a demo to see how Compose can simplify your long-term incentive plan management.

Also, check out our guide to compensation management.